")

Promote The Fiduciary Standard")

In The Best Interest Of 401k Retirement Savers?")

The Box Thinking About Non-Traditional Employee Benefits")

")

Click this Picture to go to the Retirement Readiness Calculator (a separate window will open)

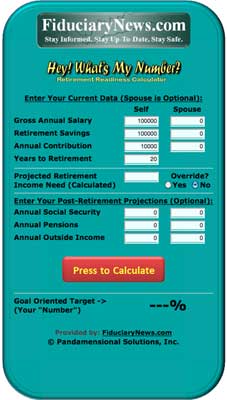

Say “hello” to your little friend to the left here. From here on, you and he will be taking on various journeys and explorations. You won’t discover hidden civilizations or alien life forms, but you may just uncover the path to a comfortable retirement. This is what I call the Hey! What’s My Number? Retirement Readiness Calculator. The real thing is a little bit more colorful. It’s available on various websites and the logo may be different. If you’re curious, this is the original – the one that started it all!

I developed this for my large group presentations. The Retirement Readiness Calculator allows everyone in the audience to pull out their smart phone, tablet or laptop computer and play along with me. In this way, I rely less on the PowerPoint (if you don’t know why that’s important, re-read the Preface of this book) and more on the audience having fun putting in their own numbers.

And just what are those numbers? Well, they’re all pretty much at your fingertips. They could be your weekly paycheck, your annual W-2 Form or your periodic 401k participant statement. To get started you want to collect the most recent figures of the following data:

- Current Annual Salary – This is quite simply the gross (i.e., before the government takes out any taxes) amount you get paid every year. You cen get this from your annual W-2 form. From this we’ll determine your projected annual retirement income need by multiplying this number by 80% (see previous chapter).

- Current Value of All Retirement Savings – This is literally all your retirement savings. Include your current employer’s 401k, any 401k’s you’ve left at companies you used to work for as well as any IRAs of any type. You can also include taxable savings and investment accounts (like what you might have at a bank, broker or mutual fund if you intend to use that money for retirement). As such, this information comes from a variety of sources, including your periodic 401k statement, any relevant brokerage or mutual fund statement and any relevant bank statements. One thing not to include here is money from “rainy day” (i.e., emergency) accounts, college savings accounts or any other pre-designated short-term savings needs.

- Current Annual Contribution – This is going to be equal to both your annual contribution and your company’s annual matching contribution. Most people forget to put in the company match. In fact, most people have forgotten what the company match is. If this isn’t easily identifiable from your periodic 401k statement, now is a good time to give your HR department a call to ascertain how much money your company is contributing on your behalf.

- How Many Years Until Retirement – Under the current rules with Social Security, you can begin taking out money at age 62, but you’ll get a bump-up if you wait until your either 66 or 67 years-old (depending on when you were born) . This is what Social Security considers the “normal” retirement age. There’s another bump-up at age 70, so there’s an extra bonus for waiting.

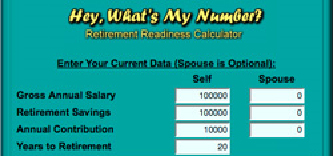

You’ll want to enter these numbers in in the appropriate spaces on the calculator. I’ve chopped up my graphic of the calculator to show you specifically where you can enter the data. As you can see, I’ve even  set aside a column for your spouse’s data if you’re married. Note you only have one space to enter in years until retirement. Now, I know what you’re thinkin,’ “What if my spouse doesn’t retire the same year I do?” Well, since we’re concerned with you (and only you) enter in the number of year you have until you retire.

set aside a column for your spouse’s data if you’re married. Note you only have one space to enter in years until retirement. Now, I know what you’re thinkin,’ “What if my spouse doesn’t retire the same year I do?” Well, since we’re concerned with you (and only you) enter in the number of year you have until you retire.

You might notice the section underneath. This contains your Projected Retirement Income Need. Your Retirement Income Need is equal to your annual expenses that occur once you retire. Don’t enter anything in here yet. The calculator will automatically ![]()

![]() determine this figure and display once you hit the “Press to Calculate” button. The automatic calculation uses the 80% Rule we discussed in the previous chapter. The rule takes your Gross Annual Salary (which you entered in the first line) and multiplies it by 80%. That’s the number that appears here. I’ve included the Projected Retirement Income Need for two reasons: one, to show you its value so you can determine if it makes sense given your own familiarity with your annual expenses; and, two, so you can override it if you feel your retirement expenses will be significantly more or less that what’s derived from the 80% Rule.

determine this figure and display once you hit the “Press to Calculate” button. The automatic calculation uses the 80% Rule we discussed in the previous chapter. The rule takes your Gross Annual Salary (which you entered in the first line) and multiplies it by 80%. That’s the number that appears here. I’ve included the Projected Retirement Income Need for two reasons: one, to show you its value so you can determine if it makes sense given your own familiarity with your annual expenses; and, two, so you can override it if you feel your retirement expenses will be significantly more or less that what’s derived from the 80% Rule.

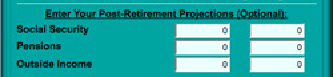

The next section of the calculator contains places to outside annual income sources. These would include income that you would receive from sources other than your own retirement savings. We don’t include inheritance, lottery winnings or any other one-time lump sum payments because they can go immediately into that pile of money you have designated to pay for your retirement. (In other words, you can save money for retirement both in tax deferred vehicles like IRAs and 401k plans, and you can also save money for retirement in regular taxable accounts like bank accounts, brokerage accounts or mutual fund accounts.)

The most likely source of outside income comes from Social Security. The Social Security Administration used to mail your current expected payments based on various retirement ages every year on your birthday.  Now you can go on-line and get that information. Enter the annualized figures from both spouses if you’re married. (Remember, Social Security reports what it pays you on a monthly basis. You’ll need to take that number and multiply it by 12 to get the number you’re supposed to enter here.) The next most likely source of outside income is a pension plan. Fewer and fewer companies have these, but many government workers still have them. Again, if this number is reported as a monthly payment, you’ll have to multiply that number by twelve and enter the result in the calculator. This line also contains room for both spouses. Finally, I included a generic “Outside Income” line. As before, you’ll need to annualize the total outside income by multiplying any monthly data by 12. You’re now ready to proceed to the part everyone’s been waiting almost 200 pages to do.

Now you can go on-line and get that information. Enter the annualized figures from both spouses if you’re married. (Remember, Social Security reports what it pays you on a monthly basis. You’ll need to take that number and multiply it by 12 to get the number you’re supposed to enter here.) The next most likely source of outside income is a pension plan. Fewer and fewer companies have these, but many government workers still have them. Again, if this number is reported as a monthly payment, you’ll have to multiply that number by twelve and enter the result in the calculator. This line also contains room for both spouses. Finally, I included a generic “Outside Income” line. As before, you’ll need to annualize the total outside income by multiplying any monthly data by 12. You’re now ready to proceed to the part everyone’s been waiting almost 200 pages to do.

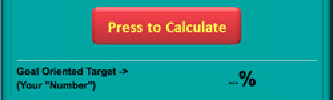

Here you go. The last section of the calculator contains on simple data output – your Goal-Oriented Target (your “number” from the title Hey! What’s my Number. Once all the above data is entered, just hit the “Press to Calculate” button. It’s a big button. You  can’t miss it. After everything has been entered in the data fields provided, you’ll want to touch the “Press to Calculate” button and watch what percentage appears next “Goal-Oriented Target -> (Your “Number”).

can’t miss it. After everything has been entered in the data fields provided, you’ll want to touch the “Press to Calculate” button and watch what percentage appears next “Goal-Oriented Target -> (Your “Number”).

I’d like to comment on one question many financial planners might ask at this point: What about inflation? If you notice, this calculator does not account for inflation. There are several reasons for this. First, any across-the-board inflation assumption would be iffy at best. Second, as alluded to in the book Your Money or Your Life, (Joe Dominguez and Vicki Robin, Penguin Books, 1993), retirees often find adequate substitutes to escape the price increases measured by inflation indices. Third, you should review your retirement readiness at least yearly. These annual reviews automatically take into consideration the impacts (if any) of inflation through rising salaries, rising contribution rates and rising required income objectives. Finally, as Andrew Carrillo, President of Barnett Capital Advisors in Miami, Florida says in “Has the 401k Fiduciary Unknowingly Put Employees in Peril?” (FiduciaryNews.com, June 10, 2014) , you can simply add your inflation assumption to your GOT to get an inflation adjusted GOT. I don’t recommend this because it’s not based on real numbers (it is, after all, an assumption) and may generate misleading results. Better to just diligently update things on an annual basis and let nature take its course.

Great! You now have your own personal “Number” for retirement. How do you know it’s good and what can you do about it if it isn’t good. The articles “How Does Goal-Oriented Targeting Work?” (FiduciaryNews.com, July 15, 2014), “Why a 401k Fiduciary Must Convince Retirement Investors to Avoid Thinking in Lump Sum Terms,” (FiduciaryNews.com, July 29, 2014), “How a Fiduciary Can Assess a Retirement Investor’s GOT,” (FiduciaryNews.com, August 5, 2014) and “5 Things to Do to Improve a Retirement Investor’s Goal-Oriented Target,” (FiduciaryNews.com, August 12, 2014) provide the answer.

Thank you, Chris